- March 22, 2022

- Posted by: Acumen

- Category: Articles, Valuation

The International Valuation Standards Council (‘IVSC’) is a not-for-profit organisation that acts as the global standard setter for the valuation profession, serving the public interest.

The IVSC is a leader in the mission to raise standards of international valuation practice and is overseen by an independent board of global leaders. Its core objectives are to:

- Develop high quality International Valuation Standards (‘IVS’) which ensure consistency, transparency and confidence in valuations throughout the world, and;

- Encourage the adoption of IVS, along with valuation professionalism provided by Valuation Professional Organisations throughout the world.

The IVS are set by the IVSC in 2013 and revised in 2017 and 2020. Independent technical standards board comprising specialist valuation experts from around the world lead the development of and consultation on IVS.

IVS are globally agreed, high-level standards which underpin valuation for all asset types. They establish a consistent and transparent framework for valuation practice worldwide.

IVS are adopted or recognised by valuation professional bodies, user groups and financial regulators around the world. As their use grows, IVS are playing an important role in supporting business and de-risking financial markets for the public good.

IVS has been divided into three parts: Framework, General Standards and six Asset-specific Standards:

IVS Framework:

This portion of the IVS is more of a preamble and explains the general principles to be followed by the valuer. Following are the contents of IVS framework:

IVS General Standards:

The General Standards set requirements for the conduct of all valuation assignments including establishing the terms of a valuation engagement, bases of value, valuation approaches and methods, and reporting.

- IVS 101 Scope of Work- This standard describes the fundamentals of engagement such as purpose of valuation, assets to be valued, period of valuation, responsibility of parties involved in valuation and other such necessary information listed below:

- Identity of the valuer;

- Identity of the clients;

- Identity of other intended users (if any);

- Asset(s) being valued;

- The valuation currency;

- Purpose of the valuation;

- Basis/ bases of value used;

- Valuation date;

- The nature and extent of the valuer’s work and any limitations thereon;

- The nature and sources of information upon which the valuer relies;

- Significant assumptions and/ or special assumptions;

- The type of report being prepared;

- Restrictions on use, distribution and publication of the report; and

- That the valuation will be prepared in compliance with IVS and that the valuer will asses the appropriateness of all significant inputs.

- IVS 102 Investigations and Compliance- As per this standard, the valuation shall be conducted in accordance with the IVS. The investigations done for valuation must be appropriate for the purpose of the valuation and basis of valuation. If the investigation doesn’t provide valuer with credible results then the valuation assignment will not comply with IVS. The valuer must comply with all the standards presented by IVS and if any other statute, law or regulatory requires any different approach then the valuer shall comply with them and this valuation will also be deemed to comply IVS.

- IVS 103 Reporting- This standard talk about how the valuer shall make the valuation report. It applies to all types of valuation reports and the valuer should provide all the necessary information that affects the valuation.

- IVS 104 Bases of Value- This mandatory standard defines the premises on which the reported values will be based. It is necessary that these bases shall be appropriate and as per the purpose of the valuation as it may influence the valuer’s selection of methods, inputs and assumptions, and ultimate opinion of value. IVS defined bases of value are as followed:

- Market value – Market rent

- Equitable value investment – Value/ worth

- Synergistic value – Liquidation value

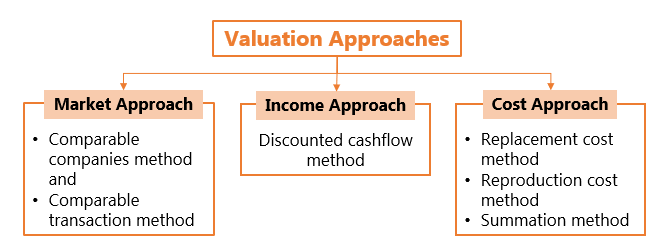

- IVS 105 Valuation Approaches and Methods- IVS has prescribed three approaches that a valuer can use to value various types of assets. Based on the asset type and availability of data, valuer can decide which approach to be used to value the asset. Those three approaches are Market Approach, Income Approach and Cost Approach. These approaches provide a valuer with certain methods to be applied for valuing the assets and are explained below:

- Market approach: This approach is based on the market data of the similar asset that is being valued. It can be based on a recent transaction where the subject asset has been sold. This approach suggests two methods; Comparable Companies Method (‘CCM’) and Comparable Transactions Method (‘CTM’). Under CCM, listed comparable companies that are actively traded in the market are considered for valuing the subject company. Under CTM, transactions of the similar or comparable asset to the subject asset are considered for valuation. (add link to the article on CCM and CTM)

- Income approach: As the name of this approach suggests, this approach is based on the forecasted cash flows that will be discounted to a net present value using an appropriate discounting rate. This approach defines a frequently used method known as discounted cashflow (‘DCF’) method. DCF principally discounts back the future cash flows to the valuation date and for long time assets it may include a terminal value which is the value of cash flows that will be generate by the asset after the forecasted period. For more information on DCF, tap on the link (add link).

- Cost approach: This approach is based on the fact that an investor will pay an amount at least up to the cost of the subject asset. This cost represents the cost that will be needed to replace or reproduce the subject asset. IVS prescribes three methods under this method, namely:

- Replacement cost method applies where we know the cost of replacing the asset with a similar modern asset either through constructing or buying the asset.

- Reproduction cost method applies where the subject asset’s replica is to be created.

- Summation method also known as the underlying asset method primarily used for investment companies is the summation of all the holdings/ underlying assets.

IVS Asset Standards: In this section, IVS defines the valuation process and approaches to be considered while valuing certain specific assets. Listed below are the standards addressing those assets:

IVS 200 Business and business interests: This standard puts light on the asset under valuation and that it should be valued in line with the purpose of valuation. This standard states specific requirements for valuing the businesses and business interests. There are various types of businesses and a valuer shall follow an appropriate approach to value them as stated under this standard.

IVS 210 Intangible assets: This standard specifically describes the methods to be followed to value various types of intangible assets and to know more about how to value intangibles visit our website (add link)

IVS 220 Non-Financial Liabilities: In this standard we get to know specific approaches and methods in details for valuing the non-financial liabilities and if there is a contradiction between this standard and the general standards, this standard shall prevail.

IVS 300 Plant and equipment: In addition to the general standards, this standard states additional principles, modifications, and some specific examples related to the valuation of plant and equipment.

IVS 400 Real property interests: This standard again gives some additional requirements which are to be followed by the valuer such as a valuer shall be familiar with the legal framework, law, and jurisdiction of the state for the real property.

IVS 410 Development property: This standard defines the development property as interests where redevelopment is required for achieving the higher standards, or where improvements are under consideration. This standard states additional requirements and modifications over and above the general standards.

IVS 500 Financial instruments: As per the subject standard, “financial instruments is a contract that creates rights or obligations between specified parties to receive or pay cash or other financial consideration”. This standard is similar to other specific standards and gives modifications, additional requirements, and some specific examples over and above the general standards on financial instruments.